The small cap growth market fared well in the third quarter, but the biggest gainers were speculative companies with weak fundamentals. We expect the rally will broaden out going forward.

Please see below for a discussion of the Osterweis Opportunity Fund’s recent performance and our near-to-medium term market outlook.

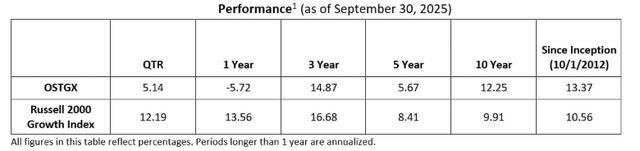

Market Recap

The third quarter was another favorable stretch in the markets, as corporate earnings were strong and economic fundamentals remained robust. In addition, the Federal Reserve cut rates by 25 basis points, which was a tailwind for both stocks and bonds.

The Russell 2000 Growth Index had a particularly bullish quarter, returning 12.2%, which was its second consecutive quarter returning 12%. It also again outpaced the S&P 500 (SP500), (SPX), which returned 8.1%. However, during the past two quarters combined, the majority of the gains in the index have been driven by speculative companies with weak fundamentals. Specifically, companies with no profits and the highest P/E ratios have delivered the strongest performance. Some of these companies benefited from a short squeeze, which drove up prices as short sellers became forced buyers, and others simply rose based on thematic momentum and market hype.

The Osterweis Opportunity Fund had a solid quarter, gaining 5.14%, but it lagged the index as we avoided speculative winners, including most biotechs and companies focused on quantum computing. We have always believed that valuation discipline is a foundation of successful investing, and we also generally avoid businesses that are not profitable. As a result, we missed some of the upside of the past two quarters, but our long-term record validates our approach, as we have substantially outperformed the index since the strategy’s inception and over the past ten years.

Portfolio Attribution

Security Selection

Our underperformance during the quarter was primarily driven by security selection, particularly our picks in Health Care, Consumer Discretionary, and Information Technology. Our holdings in Consumer Staples, Industrials, and Real Estate outperformed the index but not enough to offset the sectors that lagged.

Our Health Care stocks performed worst on both an absolute and relative basis, and our biggest negative contributor was PROCEPT BioRobotics (PRCT), a provider of robotic systems to treat benign prostatic hyperplasia (BPH) disease. The company had a poor quarter due to confusion around a C-suite shakeup. Their longtime CEO decided to retire at the same time the COO left the company. PROCEPT chose Larry Wood, an industry veteran who led a very successful transcatheter aortic valve replacement program at Edwards Lifesciences (EW), to take over as CEO, which was disappointing to the COO, who wanted the CEO job. The optics were not good, but we are delighted to have Wood as the CEO of the company. We believe the company will have strong Q3 results next month. This should allow investors to regain confidence that it is business-as-usual at PROCEPT.

Artivion (AORT), a medical device company that provides niche products to treat cardiovascular disease, was our largest contributor in Health Care. The company reported strong Q2 results, driven by an inflection in sales of their Onyx heart valve. Growth of this product accelerated to 26% from 12% in the first quarter due to clinical data that came out at the beginning of the year. The device is a major upgrade over the current standard of care because it provides the benefits of a mechanical heart valve (longevity) without the downside of needing a steady supply of blood thinners. The product carries high gross margins and is sold by an existing sales force, so the incremental profits are high. We think the company is undergoing a discovery period as investors begin to appreciate the emerging growth story.

In Consumer Discretionary, our biggest detractor was Duolingo (DUOL), the online platform for learning new languages. User growth stalled in the second quarter and continued at a stagnant pace in the third quarter. What started as an AI backlash that we expected to end quickly turned into a multi-month headwind, and we lost confidence in management’s stated goal of tripling its paying subscriber base, so we exited the stock.

Our biggest contributor in Consumer Discretionary was Boot Barn (BOOT), a retailer specializing in Western wear, cowboy boots, and other related merchandise. The company reported solid second quarter results and raised its full-year guidance. We have been impressed with the new CEO’s ability to generate consistent same store sales growth, and the company has been highly effective at navigating the current tariff environment. That said, we exited the position as the company’s market cap has increased dramatically in the past few months, and we felt most of the upside we were anticipating when we acquired the stock had already been realized.

Information Technology mildly detracted from our relative performance in the third quarter, with strong returns in semiconductors offset by weakness in software. This aligns with the macro trends, as the IT landscape bifurcated during the period. Companies providing the foundational infrastructure for AI fared well, while investor sentiment turned negative for traditional software companies. The secular demand to train and deploy increasingly complex models has continued to drive robust tailwinds for the semiconductor and high-speed connectivity sectors, and we have been leaning into the profitable companies in this space. At the same time, we have been avoiding the AI names that are experiencing top line growth but still losing money.

Monday.com (MNDY), a cloud-based software platform that allows teams to build custom project management and workflow applications, was our biggest detractor in Technology. Despite reporting relatively strong results, the company’s stock fell sharply during the quarter. The decline was triggered by a softer growth outlook and weakness in customer acquisition due to recent Google (GOOG, GOOGL) algorithm changes prioritizing AI-generated natural language summaries rather than traditional paid search links. We had been trimming the position before the company announced earnings, and we exited post-earnings due to the potential risk of disruption from AI.

Our biggest contributor in IT was Rambus (RMBS), which provides high-performance semiconductor products, playing a crucial role in data center memory and connectivity. Its Q2 report featured a powerful 43% year-over-year growth in product revenue, fueled by continued market share gains and strong demand for its DDR5 memory interface chips used in servers. In addition to its core memory interface chips, Rambus is launching three new companion chips, and management expects continued strong growth. The memory market is experiencing strong momentum, driven by rising demand from AI inference workloads — underscored by OpenAI’s recent collaboration with Samsung (OTCPK:SSNLF) and SK Hynix (OTCPK:HXSCF) to ramp up production of advanced memory chips.

Our selections in Consumer Staples performed best on a relative basis, and one of our biggest contributors was Vital Farms (VITL), an ethical egg and dairy producer, which reported a solid second quarter with a top and bottom line beat and a full-year guidance raise. We believe there remains meaningful untapped market demand for Vital’s pasture-raised egg products, and we anticipate their market share will continue to increase. With the company past its supply crunch caused by demand outstripping capacity, we believe the company is set to see accelerating revenue and profit growth when it reports third quarter results, and we hope for updated long-term guidance by their fourth quarter earnings call. We did not have any laggards in this sector.

Industrials was another area of relative strength for us, and our biggest contributor was CECO Environmental (CECO), a provider of equipment to treat wastewater as well as contaminants at manufacturing and power plants. The company had strong Q2 results supported by sales growth of 35% and order growth of 95%. Orders were buoyed by a large power infrastructure project, more of which are expected in the coming quarters. CECO is also seeing strength in the Middle East/Asia for various wastewater projects. We continue to think this is an undiscovered gem benefiting from themes like near-shoring, data center development, and the need for more power infrastructure.

Our biggest detractor in industrials was Trex (TREX) Company, a leader in composite decking, which had a poor end to the quarter driven by rumors that its key competitor, James Hardie Industries (OTCPK:JHIUF), was offering customers more aggressive discounts/rebates. After discussing this with both companies and several distributors, we believe these rumors are unfounded and driven more by investors taking certain comments out of context. Unfortunately, housing-related stocks remain out of favor, so there is a “shoot first, ask questions later” dynamic at play. We expect Q3 results to be solid, supported by dealer surveys, so we remain invested in the position.

Sector Allocation

Sector allocation was a small drag on our relative performance during the third quarter. Our underweight to Financials and zero weight in Communication Services were both additive, but our underweight to Industrials, overweight to Consumer Staples, and zero weight in Materials detracted from returns versus the index.

Portfolio Positioning & Outlook

In the near term, we expect the recent speculative fervor that has been driving small cap growth stocks will abate, and the rally will expand to companies that are showing sales and earnings growth. Additionally, we anticipate an increase in opportunities in our universe, as large structural technology shifts (e.g., mobile phones, eCommerce, and now, AI) have historically benefited large cap markets first and then worked their way down to small caps. We have already seen that trend begin to play out, and we expect it will continue as smaller, innovative companies learn how to leverage AI to create targeted, business-specific applications.

Also, we feel that a more accommodative Fed policy should allow small cap stocks to continue to rally. In the meantime, we will keep searching for high quality, reasonably valued small cap companies with long runways for organic, rapid growth.

We thank you for your continued confidence in our management.

James Callinan, CFA

Chief Investment Officer – Small Cap Growth

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here